As a sub-sector of the mortgage-backed securities (MBS) market, affordable housing offers additional diversification due to particular characteristics attributable to the affordable housing sector. Generally, that the MBS sector has benefited from strong U.S. real estate fundamentals and favorable supply/demand dynamics; further, the affordable housing sub-sector also benefits from the support of federal low-income housing tax credits (LIHTC) and steady demand for low-income housing. The results have demonstrated solid historical asset performance through real estate cycles with relatively low correlation to other asset classes.

Low Correlation: In our view, the features specific to MBS—like prepayment, underlying credit quality, and duration/convexity—contributed to the relatively low correlation of MBS to other fixed-income sectors. We also believe that the particular characteristics of affordable housing investments act as a diversifier even within the MBS sector.

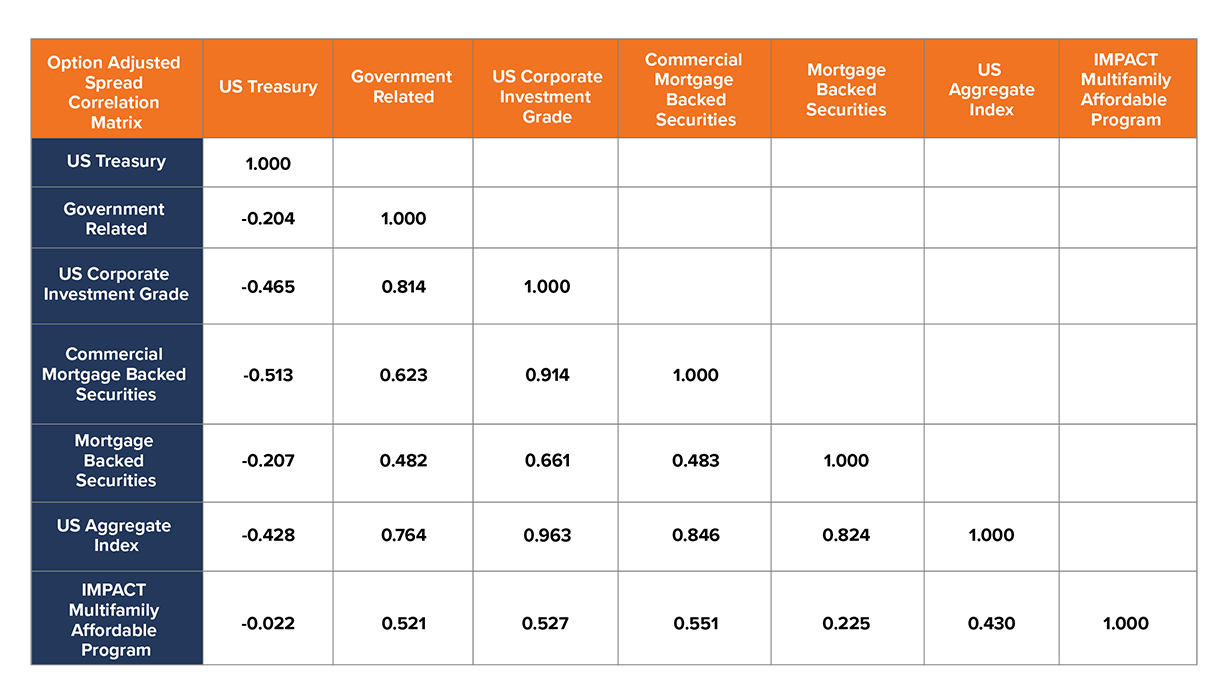

As the chart below shows, since 2008, IMPACT’s affordable housing sector’s spread levels or loan yields over Treasury rates have had relatively low correlations to other bond sectors in the Bloomberg Barclays US Aggregate Index1.

Cyclicality: Cyclicality refers to the fluctuating appetite for certain types of risks and excess returns generated by various spread products. We believe that the cyclicality of MBS’ excess returns tends to provide a somewhat differentiated pattern of returns than those of U.S. governments and credits.

LIHTC-eligible affordable housing developments have had much lower default rates than traditional multi-family housing projects over the past twenty years. In our view, this is due in part to the equity structure of LIHTC-eligible housing developments, as project stakeholders are incentivized to keep a loan out of default to retain the tax credits over the life of the loan.

Interest Rates: MBS’ risk of prepayment increases when interest rates decline and decreases when rates rise. Borrowers tend to refinance when rates decline resulting in early principal payment to investors who in turn are left to reinvest this cash in another security with a potentially lower yield.

As we see it, the prepayment characteristics of the affordable housing mortgages collateralized by LIHTC-eligible affordable housing developments are more favorable because they typically contain provisions to limit prepayment. These provisions create an investment that can have positive convexity with a corresponding longer duration since borrowers typically will not prepay as quickly as traditional MBS borrowers. We believe that this creates an attractive long-term investment for institutions with long duration liabilities such as pension funds or life insurance companies.

Over the past 20 years, IMPACT’s investment approach has been to consistently deliver market rate returns and below-industry-standard default rates. To date, IMPACT has financed over 45,000 units of affordable housing by investing over $1 billion of institutional assets in affordable housing loans.

We know that every investment requires a thorough risk/benefit analysis. When examining the affordable housing sector, we believe that institutions can tap into “positive returns”2—value that rewards not only their investors but underserved communities alike.

Thoughts? We’d love to hear from you at info@impactcapital.net.

1 Source: Bloomberg Barclays with calculations by IMPACT using Option Adjusted Spread

2 Please note that “Positive Returns” is not a guarantee of any kind but rather a term of art. “Positive Returns” means investing with the intent of generating measurable social change, in addition to financial returns, and realizing the intangible benefits of being viewed as a good corporate citizen by our investors’ constituents. Investors are subject to the risk of loss. anticipated. Past performance is no guarantee of future results. Use of this document is subject to the terms and conditions set forth on Impact Community Capital LLC’s website and can be accessed at http://impactcapital.net/about/terms-and-conditions/.